DESCRIPTION

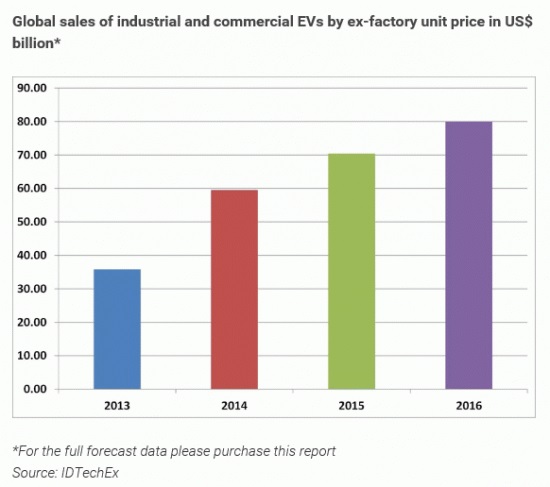

Those selling components for electric vehicles and those wishing to make the vehicles themselves must seek where the majority of the money is spent and will be spent. That must lead them to industrial and commercial electric vehicles because today these represent 60% of the value of the electric vehicle market. Indeed, this sector is set to grow 4.5 times in the next decade. Industrial and commercial electric vehicles include heavy industrial vehicles, the term referring to heavy lifting, as with forklifts.

Then we have buses, trucks, taxis and the other light industrial and commercial vehicles. There are also a few work boats and commercial boats and one day there will be commercial electric aircraft but this is really a story about the burgeoning demand for off-road industrial vehicles and on-road commercial vehicles. In particular, industrial electric vehicles make industry more efficient and commercial electric vehicles reduce congestion. Both of them greatly reduce pollution and align closely with government objectives concerning industry and the environment, yet they minimally depend on subsidy, in contrast with some other electric vehicle types.

This report covers the technical and market trends for industrial and commercial vehicles whether hybrid or pure electric, putting it in the context of electric vehicles overall and including the activities of a host of manufacturers of the vehicles and their components and even providing future technological development roadmaps.

The market for electric industrial vehicles is already large because, by law, forklifts have to be electric when used indoors. Little growth remains in this market but outdoors almost all earthmoving and lifting vehicles use the conventional internal combustion engine. That is about to change dramatically because hybrid electric versions reduce cost of ownership and exposure to price hikes with fossil fuels. Hybrids increasingly perform better as well, with more power from stationary, ability to supply electricity to other equipment and other benefits including less noise and pollution. On the other hand, airports, often government owned or funded, are under great pressure to finish converting their Ground Support Equipment GSE to pure electric versions both on and off the tarmac partly using federal grants.

Yet another industrial trend is for use of electric vehicles to replace slow and often dangerous manual procedures. Sometimes a self-powered indoor crane replaces scaffolding. An electric stair climber replaces human effort and possible injury. On the other hand, sit-on floor cleaners in buildings, sit-on ice cleaners in ice rinks, outrider vehicles carried on trash collection trucks and a host of similar solutions speed processes and reduce injuries and costs.

Buses, trucks, taxis and the other light industrial and commercial vehicles are going electric for similar reasons but we must add the desire of national and local governments, who buy many of them, to go green, even where there is no payback. However, the size and growth of the industrial and commercial sector is less dependent on government funding and tax breaks than the more fragile market for electric cars, particularly pure electric ones. Excitingly, most of the electric vehicle technologies are changing and improving hugely and innovation often comes here before it is seen in the more publicised electric vehicle sectors such as cars.

Asynchronous traction motors were first widely used on forklifts: their benefits of longer life, less maintenance, low cost and freedom from magnet price hikes and heating problems are only later being seen in a few cars. Ultracapacitors otherwise known as supercapacitors permit very fast

charging of buses whether by the new Level 3 charging stations or regenerative braking and they release huge surges of power when the bus is full and starting on a hill. Gas turbine range extenders have been on some buses for 12 years but they are only now being planned for cars. Fuel cells will be viable in fleets where the expensive hydrogen distribution is manageable - not for cars across the world. Energy harvesting shock absorbers about to hit the market will be very viable on buses and trucks where they can put up to 12 kW into the battery whereas such devices on cars will take longer to prove.

Nevertheless, it is important to look at industrial and commercial electric vehicles as part of all electric vehicles out there - as we do - because it is increasingly true that one company will produce EVs for many end uses and even make key components. This achieves the product reliability and cost advantages that come from highest volume manufacture based on standardisation and shared research.

Analyst access from IDTechEx

All report purchases include up to 30 minutes telephone time with an expert analyst who will help you link key findings in the report to the business issues you're addressing. This needs to be used within three months of purchasing the report.

Table of Contents

1. EXECUTIVE SUMMARY AND CONCLUSIONS

1.1. Dominant electric commercial vehicle types and influences change

1.2. Market forecasts

1.3. IDTechEx forecast for commercial vehicles 2017-2027

1.4. Latest progress

1.5. Examples of new industrial and commercial vehicles and projects announced in 2016

1.5.1. Powertrain choices change radically

1.6. Electrical machine systems take more cost, batteries less

1.7. The elephant in the room: conventional vehicles

1.8. News in 2016

1.8.1. June 2016

1.8.2. July 2016

1.8.3. August 2016

1.8.4. September 2016

1.8.5. October 2016

1.8.6. November 2016

1.9. Buses will be taxis will be buses

1.10. Powertrain situation in 2017

1.10.1. Leaders of change, move to hybrids

1.10.2. Move to 48V mild hybrids

1.10.3. Move to autonomy

1.10.4. Volvo electrification of mining vehicles

1.10.5. Forklifts change little

2. INTRODUCTION

2.1. Urban logistics trends

2.2. Technology disagreement

2.3. The special case of China

2.3.1. Pollution control is urgent

2.3.2. Particulate matter - China the worst

2.3.3. Inadequate roads and parking

2.3.4. Example of action BYD

2.3.5. BYD begins expansion of manufacturing facility - September 2016

2.4. Biggest EV?

2.5. Different strategies

2.6. Battery Vehicle Work Rounds for Very Long Range

2.6.1. Light truck with fuel cell, battery and supercapacitor

2.7. Reusable electric powertrain

2.8. Here come the tougher emissions regulations

2.9. Cars are often fleets not private

2.10. US Postal Service 180,000 vehicles

3. LESSONS FROM RECENT CONFERENCES

3.1. Overview

3.2. Hydraulic vs electric efficiency

3.3. Market forecasts

3.4. Powertrain trends

3.5. Energy Independent Vehicles EIV

3.6. Projects and new industrial EVs

3.7. Wheel loaders

3.7.1. Hitachi

3.7.2. Oerlikon

3.7.3. HUDIG TIGON hybrid excavator and wheel loader

3.7.4. John Deere

3.7.5. Volvo Group

3.8. Star of the show

3.8.2. Future dreams!

3.9. Components and systems

3.9.1. Power electronics

3.10. Energy storage

3.10.1. Lithium Sulfur batteries

3.10.2. Motors

3.10.3. User needs and benefits

4. MARKET DRIVERS FOR INDUSTRIAL AND COMMERCIAL EVS

4.1. Trends

4.2. Advantages of electric commercial vehicles

5. HEAVY INDUSTRIAL EVS

5.1. What is included

5.2. Challenges

5.3. Forklifts

5.3.1. Small forklift success

5.3.2. A look at many FC forklifts across the world

5.3.3. Plug Power transforms the industry

5.3.4. Asia Pacific Fuel Cell Technologies APFCT

5.3.5. Forklift market analysis

5.3.6. FC material handling fleets and standards

5.3.7. Market analysis

5.3.8. FC material handling fleets and standards

5.4. Listing of manufacturers

5.4.1. Statistics for all types of industrial lift truck

5.4.2. Manufacturers of heavy industrial EVs

6. LIGHT INDUSTRIAL & COMMERCIAL EVS

6.1. Introduction

6.1.1. Overview

6.1.2. One quarter of commercial vehicles in Germany can be electric now?

6.2. Sub categories

6.3. Local services

6.4. Airport EVs

6.4.1. USA statistics

6.4.2. GSE by airline and airport

6.4.3. Here come hybrids

6.4.4. US incentives

6.4.5. Overall market

6.4.6. Airport applications widen

6.4.7. Sea-Tac Airport 2014

6.5. Small people-movers

6.6. Chrysler minivan in 2015

6.7. Dong Feng China big minivan order

6.8. Kargo Canada

6.9. Light industrial

6.10. All-terrain vehicles for commercial use

6.11. Listing of manufacturers

7. BUSES AND TRUCKS

7.1. Introduction

7.2. Summary of technical preferences

7.3. Statistics issues

7.4. Successful pure electric buses vs addressable market

7.5. Chinese price/performance

7.6. Cost trends - China ready to pounce

7.7. Market drivers and impediments

7.8. Regional differences

7.9. China, India and cities

7.10. Radical change

7.11. Truly global market for similar buses

7.12. Large pure electric buses: first big orders 2014/5

7.13. Weak trend to larger buses but not in China

7.14. Value chain and powertrain

7.15. Hybrids becoming pure electric

7.16. Relative importance of technical options

7.17. Technology disagreement

7.18. Fuel cell buses: progress and potential

7.18.1. Use of solar on hybrid fuel cell shuttle buses

7.19. Background statistics: automotive industry and buses in general

7.19.1. Automotive industry

7.19.2. School buses

7.19.3. Largest bus manufacturers

7.20. E-bus news in 2016

7.21. Trucks

7.21.1. Which Electric Truck Powertrain Wins?

7.21.2. Medium and heavy duty trucks

7.21.3. Travel through Munich in a vehicle that is 100% electric, clean, quiet

7.21.4. News in June 2016 - Mack Trucks to Evaluate Wrightspeed Route Powertrain in Mack LR Model

7.21.5. News in July 2016 - Argonne to lead consortium for new CERC medium- and heavy-duty truck technical track

7.21.6. News in August 2016 - Daimler plan heavy duty trucks

7.21.7. News in August 2016 - Fuel cell truck

7.21.8. News in September 2016 - Volvo first in the world with self-driving truck in underground mine

7.21.9. News in October 2016 - BMW i supply agreement with Workhorse Group

8. TAXIS

8.1. Electric taxi projects in China, Europe, Mexico, UK, UK, Japan

8.2. Huge order from the Philippines?

8.3. Terra Motors Interview Tokyo September 2015

8.3.1. Introduction

8.3.2. Latest market appraisal

8.3.3. View of India

8.3.4. View of Bangladesh

8.3.5. View of Vietnam

8.3.6. View of Philippines

8.3.7. View of Japan

8.3.8. IDTechEx conclusion

9. THREE WHEEL COMMERCIAL VEHICLES

9.1. Background

9.2. Three wheelers as crossover products

9.3. Operational benefit of three wheel

9.3.1. Introduction

9.3.2. Nissan DeltaWing

9.3.3. The basics driving us to three wheel

9.3.4. Energy efficiency

9.3.5. Relative magnitude of energy dissipation

9.3.6. Occupancy trend favours 3 wheel?

9.3.7. Low cost three wheel vehicle market

9.3.8. The Indian three wheel market - the largest globally

9.3.9. Electric three wheeler penetration

9.4. Benefits of three wheelers

9.5. Three wheel electric vehicles: varied positioning in the market

9.5.1. Twike, Piaggio, Xingui and others contrasted

9.5.2. Toyota scenario

9.5.3. Spira4u in 2015

9.6. Mule: Modern Electric Workhorse to Slice Through Urban Traffic Easily

9.7. Barriers for adoption of three wheel EVs

10. ELECTRIC VEHICLES FOR CONSTRUCTION, AGRICULTURE AND MINING

10.1. Overview

10.2. Value proposition and environmental restrictions

10.3. Autonomous vehicles for agriculture and mining

10.4. Energy and work synchronization in mining

10.5. Light manned vehicles - PapaBravo Canada

10.6. Examples of cranes and lifters

10.7. Caterpillar and Komatsu: energy harvesting on large hybrid vehicles

10.7.1. CALSTART partnerships

10.7.2. Other electrification of large vehicles

11. KEY COMPONENTS FOR INDUSTRIAL AND COMMERCIAL ELECTRIC VEHICLES

11.1. Types of electric vehicle

11.2. Many fuels

11.3. Born electric

11.4. Pure electric vehicles are improving

11.5. Series vs parallel hybrid

11.6. Modes of operation of hybrids

11.6.1. Plug in hybrids

11.6.2. Charge-depleting mode

11.6.3. Blended mode

11.6.4. Charge-sustaining mode

11.6.5. Mixed mode

11.7. Microhybrid is a misnomer

11.8. Deep hybridisation

11.9. Hybrid vehicle price premium

11.10. Battery cost and performance are key

11.11. Trade-off of energy storage technologies

11.12. Ultracapacitors = supercapacitors

11.12.1. Where supercapacitors fit in

11.12.2. Advantages and disadvantages

11.12.3. Can supercapacitors replace batteries?

11.12.4. Supercapacitors - a work round for troublesome batteries

11.12.5. Supercabatteries: lithium-ion capacitors

11.13. Range extenders

11.13.1. What will be required of a range extender?

11.13.2. Three generations of range extender

11.13.3. Fuel cell range extenders

11.13.4. Single cylinder range extenders

11.14. Big effect of many modest electricity sources combined

11.15. Energy harvesting

11.16. Trend to high voltage

11.17. Structural components

11.18. Trend to distributed components

11.19. Trend to flatness then smart skin

11.20. Traction batteries

11.20.1. After the shakeout in car traction batteries

11.20.2. The needs have radically changed

11.20.3. It started with cobalt

11.20.4. Great variety of recipes

11.20.5. Other factors

11.20.6. Check with reality

11.20.7. Lithium winners today and soon

11.20.8. Reasons for winning

11.20.9. Lithium polymer electrolyte now important

11.20.10. Winning chemistry

11.20.11. Titanate establishes a place

11.20.12. Laminar structure

11.20.13. Niche winners

11.20.14. Fluid situation

11.21. Traction motors

11.21.1. Overview

11.21.2. Examples of motors in action

11.22. Power electronics

12. INDUSTRIAL AND COMMERCIAL COMPANY PROFILES

12.1. Ayton Willow

12.2. Bradshaw Electric

12.3. Caproni JSC

12.4. Crown Equipment Corporation

12.5. Hyster-Yale

12.6. John Deere

12.7. Jungheinrich AG

12.8. Kion Group GmbH

12.9. Liberty Electric Cars

12.10. MAN Truck & Bus AG

12.11. Toyota Motor

12.12. Valence Technologies

12.13. VISEDO Oy

12.14. ZNTK Radom

APPENDIX - ELECTRIC AND HYBRID ELECTRIC NON-ROAD EVS NOW AND IN FUTURE

IDTECHEX RESEARCH REPORTS AND CONSULTANCY

TABLES

1.1. Numbers of industrial & commercial EVs, in thousands, sold globally, 2017-2027

1.2. Unit prices, ex factory, of industrial & commercial EVs, in US$ thousands, globally, 2017-2027

1.3. Market value of industrial & commercial EVs, in US$ billions, sold globally, 2017-2027

2.1. Examples of very different bus and freight solutions for essentially the same types of vehicle and some of the relative benefits and challenges. Commonalities highlighted in color.

4.1. Some reasons why ICE vehicles are replaced with EVs

4.2. Advantages of pure electric commercial vehicles, enjoyed to some extent by hybrid electric versions

4.3. Potential challenges of electric commercial vehicles

5.1. 27 examples of manufacturers of heavy industrial EVs by country

6.1. 150 manufacturers of light industrial and commercial EVs and drive trains by country and examples of their products

7.1. Market for conventional diesel buses, hybrid and pure electric buses > 8t by rationale, end game in green

7.2. Price spread $K of buses >8t by region and technology 2012 and 2015, with exceptional prices excluded. High priced market red. Low priced market green. Significant price decrease bright green.

7.3. Market drivers and impediments are summarised below.

7.4. Advantages of pure electric buses, enjoyed to some extent by hybrid electric buses

7.5. Market drivers of future purchasing of buses by region and % growth. Green shows strongest market drivers

7.6. League table of EV traction battery manufacturers mWh

7.7. The typical chassis-plus-body value chain of hybrid buses 2015. Main added value shown in green

7.8. Trend of pure electric bus value chain - integral bus

7.9. Trend of pure electric bus value chain - integral bus with structural electronics

7.10. Some of the main technological options compared

7.11. Examples of very different bus and freight solutions for essentially the same types of vehicle and some of the relative benefits and challenges. Commonalities highlighted in color.

7.12. Some of the factors increasing pure electric bus range 2017-2027

7.13. e-bus drive train technology options compared, with commercially problematic issues highlighted

7.14. 2012 and 2013 production of heavy buses by country from OICA correspondents' survey

7.15. Second quarter YTD 2014 and 2013 production of heavy buses by country

7.16. School bus statistics for USA and China 2015

7.17. First half sales by country for commercial vehicles CV 2013/3/4

7.18. Top five bus manufacturers 2005, 2011, 2015, Chinese in red, with output number of buses >8t

7.19. Domestic bus sales in China in October 2014

7.20. Rank of automotive manufacturers by production in 2013. LCV includes Minibuses," derived from light commercial vehicles, are used for the transport of passengers, comprising more than eight seats in addition to the driver's seat a

7.21. Examples of E-bus news in 2016 with IDTechEx comment

8.1. 19 projects testing pure electric taxis

9.1. Domestic sales by category in India

9.2. Planned Deployment of Electric 3 wheelers in India

11.1. Three generations of range extender with examples of construction, manufacturer and power output

11.2. Traction battery technologies in 2012, number percentage lead acid, NiMH and lithium

11.3. Traction battery technologies in 2022 number percentage lead acid, NiMH and lithium

11.4. Traction battery technology by applicational sector 2010 and 2020, examples of suppliers and trends

11.5. What is on the way in or out with traction batteries

11.6. Over 450 vertically integrated lithium traction battery cell manufacturers, their chemistry, cell geometry and customer relationships (not necessarily orders)

11.7. 68 industrial and commercial electric vehicles and their motor details.

11.8. Examples of electronics and electrics replacing mechanical parts in electric vehicles.

11.9. Examples of cost reduction of electrics/ electronics by radical alternatives.

FIGURES

1.1. Numbers of industrial & commercial EVs, in thousands, sold globally, 2017-2027

1.2. Unit prices, ex factory, of industrial & commercial EVs, in US$ thousands, globally, 2017-2027

1.3. Market value of industrial & commercial EVs, in US$ billions, sold globally, 2017-2027

1.4. Japanese strawberry picking robot

1.5. The Wall-Ye V.I.N. robot created by Christophe Millot and Guy Julien, picks grapes in a vineyard

1.6. Daimler is developing the Mercedes-Benz Future Truck 2025, an autonomous vehicle for on-road goods transport.

1.7. Peloton Technology

1.8. Domino's Pizza Enterprises announced its experimental DRU autonomous pizza delivery robot

1.9. Bonirob from Deepfield Robotics automates and speeds up analysis.

1.10. 'Dancer bus' is a project by JSC 'vėjo projektai'

1.11. Citaro will hit the market as an E-Cell (BEV), as well as a F-Cell (FCV)

1.12. View of Volvo Group on future of truck powertrains

1.13. 48V mild hybrid commercial van

1.14. Volvo Truck Technology view of 48V mild hybrid truck opportunity

1.15. Nanowinn tourist bus

1.16. UQM PowerPhaseDT

1.17. Mercedes pure electric eTruck

1.18. Charge autonomous delivery truck

1.19. Selection of IDTechEx images taken at Barclays event London September 2016

1.20. Slides from Industrial Vehicle Symposium Cologne Germany November 2016

1.21. Volvo hybrid wheel loader with Volvo autonomous pure electric carrier as prototype.

2.1. Trend of freight transport urban vs long haulage 2010-2025

2.2. Transport of people 2010-2025

2.3. LCV and urban bus usage hours

2.4. China carbon dioxide emissions vs rest of world

2.5. Green vehicles in China 2015-2020

2.6. Sales of BYD electric buses in China 2015

2.7. BYD deployment of electric taxis

2.8. BYD QIN hybrid car

2.9. Strategy of Iveco Italy in late 2014

2.10. Siemens truck charging

2.11. Siemens costings

2.12. Catenary truck charging by country

2.13. Vehicle architecture and characteristics

2.14. Effect of fuel cell on payload. Fuel cell control.

2.15. Fuel cell + supercapacitors control

2.16. Simulation comparison

2.17. Display at EVS29

2.18. Savings and benefits

2.19. Layout

3.1. Megatrends, regulations and other market drivers

3.2. CALSTART overview

3.3. Hitachi electric construction vehicles including hydraulic and electric hybrids.

3.4. Cummins hybrid electrification example

3.5. John Deere tractor electrification

3.6. Ricardo overview

3.7. AVL forecast for industrial and commercial electric, mild hybrid and conventional vehicles including rental cars

3.8. Tiny deployment of fuel cell forklifts

3.9. Sevcon fuel cell power electronics options offered.

3.10. Some targets for hybrid powertrains

3.11. Hitachi electrification of wheel loader

3.12. Oerlikon wheel loader approach

3.13. HUDIG hybrid wheel loader

3.14. John Deere hybrid wheel loader

3.15. Volvo connecte4d machines: hybrid wheel loader with Volvo autonomous pure electric carrier as prototype and pure electric excavator.

3.16. Delphi view

3.17. Thermal management of power electronics

3.18. Lithium sulfur battery target

3.19. Ricardo traction motor overview

3.20. Konecranes using supercapacitors below

3.21. Examples of hybrid options

4.1. Efficiency in power needed per person per distance for different forms of on-road passenger transport

4.2. Bus size vs fuel consumption

5.1. Caterpillar CAT series hybrid diesel electric bulldozer

5.2. Mitsubishi diesel electric hybrid lifter

5.3. Heavy electric vehicle

5.4. Toyota fuel cell forklift and other fuel cell vehicles and activities

5.5. Fuel cell forklifts from across the world

5.6. Refuelling a Plug Power unit

5.7. APFCT fuel cell forklift system showing two refueller cabinets

5.8. Top 20 industrial lift truck suppliers in 2014

5.9. World industrial truck statistics/orders and shipments

6.1. Electric bus in Nepal

6.2. Kargo Light

6.3. Mobile electric scissor lift by Wuhan Chancay Machinery and Electronics

6.4. Garbage collecting electric car

6.5. Ecovolve battery powered tip dumpers

7.1. Tata Motors CNG hybrid bus in India left and BYD K9 pure electric bus from China right that is the most widely trialled and adopted of its type

7.2. Ex-factory lowest price range of diesel, hybrid and pure electric 35-90 seat urban buses in China vs North America/ Europe 2012 and 2015. Chinese cost reduction of hybrids is obscured by move to more expensive hybrids (long range

7.3. Passenger travel by bus by region in England.

7.4. BYD articulated pure electric Lancaster bus for 120 passengers with 170 km range announced late 2014

7.5. The value chain is changing radically due to vehicle design being changed as summarised below. Ladder type hybrid bus chassis top

7.6. Structural supercapacitor as car or bus bodywork, experimental

7.7. UITP summary of technological options for buses

7.8. MAN Lion urban bus with supercapacitors and no traction battery, the favoured practice in China

7.9. EV powertrain technology roadmap

7.10. Percentage share of 92 fuel cell bus trials 1990-2015 by fuel cell manufacturer

7.11. North American sales of school buses 2000-2009, total buses sold

7.12. Top five sales volume of light bus manufacturers in November 2013

7.13. Top five sales volume of medium bus manufacturers in November 2013

7.14. Top five sales volume of large bus manufacturers in November 2013

7.15. The Nikola One has 6×6 all-wheel drive

7.16. The Extended Range Electric Vehicle EREV truck

7.17. Planned TEVA hybrid truck and JAC production line.

7.18. EDI CNG hybrid truck

7.19. The electric truck by the BMW Group and the SCHERM group

7.20. A Mack® LR® model retrofitted with the Wrightspeed Route™ 1000 powertrain

7.21. Workhorse E-Gen electric delivery vehicle

8.1. Taxi fire caused by a bad lithium-ion battery in a Chinese electric taxi

8.2. BYD taxi rollouts in late 2014

8.3. BYD Qin hybrid car

8.4. The Terra Motors e-trike

8.5. E-trikes used as taxis

8.6. Logos compared

8.7. Expensive version for developed countries and basic version for undeveloped countries

9.1. Nissan DeltaWing

9.2. Energy dissipation through air resistance

9.3. Typical Chinese three wheel on-road vehicles.

9.4. Electric Three Wheel Taxi by LangFang Sandi Electric Tricycle Co. Ltd.

9.5. Bubble e-bike

9.6. Domestic market share for 2012-13

9.7. Bajaj Auto is a dealer in the manufacturing of commercial three wheel vehicles

9.8. Bajaj Affordable Three Wheel Commercial Vehicle 2014 (2,000 usd) available in Natural Gas, Liquefied Gas and Diesel versions

9.9. Electric vehicle cost breakeven

9.10. Twike pedal-assisted electric vehicle left in Switzerland and some of the 100 Mexico City pedelec taxis right

9.11. Piaggio tilting three wheel scooters with conventional engines and below one from Xingue China

9.12. Toyota i-Road pure electric tilting three wheeler

9.13. Spira4u

9.14. Mule: Modern Electric Workhorse to Slice Through Urban Traffic Easily

10.1. Grizzly robot electric vehicle for agriculture and mining

10.2. Sanyo commercial vehicle with extending solar panels for charging when stationary and mine with electric trucks using local solar and wind

10.3. Energy and work synchronization

10.4. Pure electric light mining vehicles

10.5. Bailey hybrid electric crane

10.6. Konecranes hybrid electric stacker

10.7. Pure electric manlift

11.1. Hybrid bus powertrain

11.2. Hybrid car powertrain using CNG

11.3. Some hybrid variants

11.4. Evolution of plug in vs mild hybrids

11.5. Trend to deep hybridisation

11.6. Evolution of hybrid structure

11.7. Price premium for hybrid buses

11.8. Three generations of lithium-ion battery with technical features that are sometimes problematical

11.9. Battery price assisting price of hybrid and pure electric vehicles as a function of power stored

11.10. Probable future improvement in parameters of lithium-ion batteries for pure electric and hybrid EVs

11.11. Comparison of battery technologies

11.12. Where supercapacitors fit in

11.13. Energy density vs power density for storage devices

11.14. Indicative trend of charging and electrical storage for large hybrid vehicles over the next decade.

11.15. Evolution of construction of range extenders over the coming decade

11.16. Examples of range extender technology in the shaft vs no shaft categories

11.17. Illustrations of range extender technologies over the coming decade with "gen" in red for those that have inherent ability to generate electricity

11.18. The principle of the Proton Exchange Membrane fuel cells

11.19. Trend of size of the largest (in red) and smallest (in green) fuel cell sets used in 98 bus trials worldwide over the last twenty years.

11.20. Electric machine and ICE sub-assembly

11.21. 48V Model chosen

11.22. Evolution of traction batteries and range extenders for large hybrid electric vehicles as they achieve longer all-electric range over the next decade.

11.23. Main modes of rotational energy harvesting in vehicles

11.24. Main forms of photovoltaic energy harvesting on vehicles

11.25. Maximum power from the most powerful forms of energy harvesting on or in vehicles

11.26. Hybrid bus with range improved by a few percent using solar panels

11.27. Possible trend in battery power storage and voltage of power distribution

11.28. Volkswagen view of the attractions of 38V

11.29. Mitsubishi view of hybrid vehicle powertrain evolution

11.30. Flat lithium-ion batteries for a car and, bottom, UAVs

11.31. Supercapacitors that facilitate fast charging and discharging of the traction batteries are spread out on a bus roof

11.32. Here comes lithium

11.33. Approximate percentage of manufacturers offering traction batteries with less cobalt vs those offering ones with no cobalt vs those offering both. We also show the number of suppliers that offer lithium iron phosphate versions

Price information:

Single User License: USD4975